Introduction to the UK Power System

The UK electricity system is undergoing structural change, with 2024 marking the first year that renewable energy supplied over 50% of total generation.[1] At the same time, the phase-out of coal and rise of renewables have driven a sharp fall in power sector emissions. Between 2010 and 2024 emissions have fallen from 198 million tonnes of carbon dioxide equivalent (mtCO2-eq) to 59 mtCO2-eq, or a 70% reduction.[2] This transition has been driven by falling costs of onshore wind, offshore wind and solar PV that have been cheaper than coal and gas since before 2020. Despite this high level of renewable penetration, the UK energy grid is still reliant on gas peaking plants to balance supply and demand during energy peaks, troughs and during periods of bad weather. There are two major challenges to decarbonising the grid – under and over supply of renewable energy.

- Under-supply: When wind and solar don’t generate enough electricity, fossil fuels fill the gap, increasing carbon emissions and consumer electricity bills.

- Over-supply: When generation is greater than demand, renewable energy is curtailed in order to maintain the UK grid frequency at around 50 Hertz. In 2024, more than 10% of wind generation was curtailed.

Furthermore, renewable energy is intermittent and non-dispatchable which limits its ability to respond to real-time grid demands. Historically, balancing was provided by fossil fuel plants with dispatchable capacity, but as these decline, alternative forms of flexibility are required to deliver the fast-response and dynamic balancing services needed for system stability.

The role for LDES in Clean Power 2030

The UK has committed to achieving 95% clean electricity by 2030 and a fully decarbonised grid by 2035. Delivering this ambition will require novel and innovative energy storage technologies.[3] Long Duration Energy Storage (LDES) is uniquely positioned to bridge this gap by storing renewables for extended periods, from days up to weeks. LDES solutions could reduce energy waste, lower consumer costs and provides the grid flexibility needed to replace fossil fuels. As a result, the UK’s National Energy System Operator estimates 11.5-15.3GW of LDES capacity will be required to decarbonise the grid by 2050.[4]

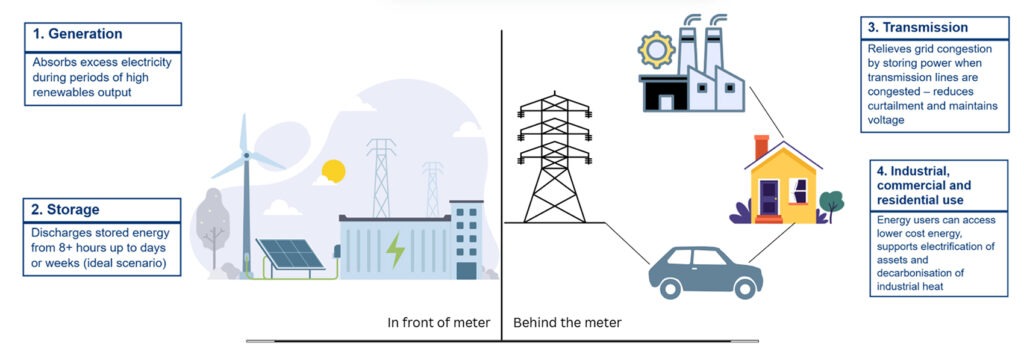

Figure 1 illustrates the multiple applications of LDES across the power system. In front of the meter, LDES can absorb excess renewable generation (1) and later discharge is over periods ranging from hours to weeks (2). At the transmission level, LDES can relieve grid congestion by storing electricity when the system is constrained – reducing curtailment and maintaining voltage stability (3). Behind the meter, storage allows commercial, industrial and residential users to access lower-cost electricity and decarbonise overall operations (4).

Current capacity and new projects

The UK currently has 2.8 GW of long-duration storage, almost all from four pumped hydro sites in remote and geographically constrained regions. To scale and meet grid demand, LDES must be deployable near demand hubs, where grid congestion and industrial load are highest.

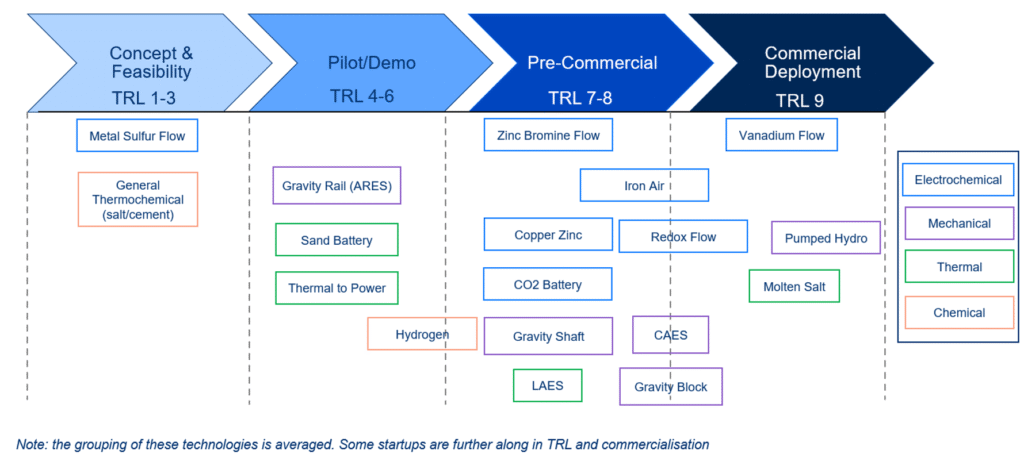

The current project pipeline is beginning to address this and a number of novel solutions are emerging across the landscape. The technological readiness level of all emerging LDES innovations can be seen in Figure 2 – from concept and feasibility (TRL 1-3), through pilot and demonstration projects (TRL 4-6), into pre-commercial trials (TRL 7-8) and full commercial operation (TRL 9).

Of these emerging technologies, some of the most promising advancements are:

- Flow batteries: Several UK companies are advancing flow battery systems that can provide 8-12 hours of storage with minimal degradation. Invinity Energy Systems, one of the UK’s first listed LDES companies, plans to deliver 20.7 MWh at its first commercial site in 2026. Innovators like RFC Power are developing alternative chemistries like hydrogen-manganese, promising high round-trip efficiency and lower storage costs, even compared to Li-ion battery systems.

- Air Energy Storage: Compressed air (CAES) and liquid air (LAES) technologies store energy by pressuring or cooling air, then re-expanding it to generate electricity. Highview Power is building a 300 MWh LAES facility near Manchester with further projects planned across Scotland. Keep Energy Systems are piloting modular CAES with integrated thermal storage for industrial and community-scale applications.

- Thermal Energy Storage (TES): TES has the unique ability to decarbonise heat-intensive industries like glass, cement and steel where temperatures exceed 1500°C. TES can convert surplus renewable electricity into heat stored in mediums such as molten salt and ceramic blocks – which can later be used directly in industry or reconverted to power. Companies like Exergy3 are developing ceramic bricks that store heat at over 1,200°C.

LDES versus Li-ion solutions

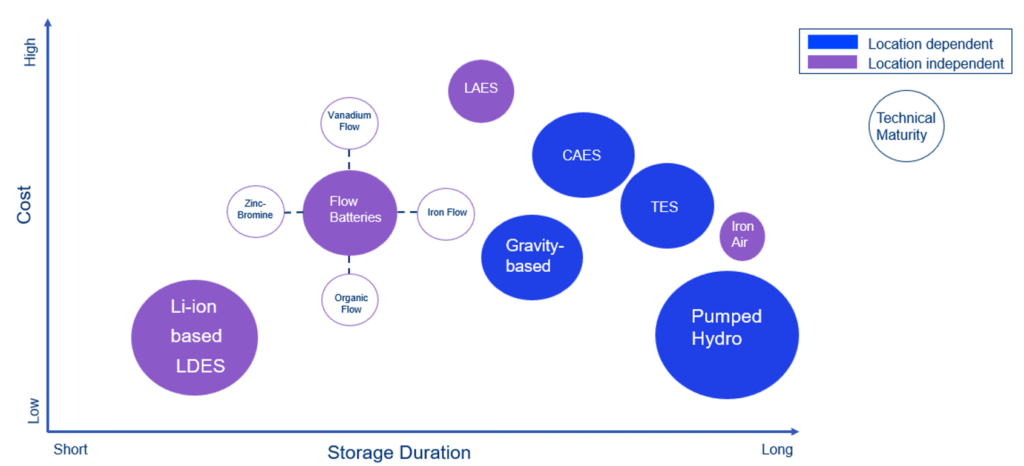

One of the key challenges to commercialising LDES is the dominance of li-ion in today’s market, particularly for storage durations of 1-4 hours. Over the past decade, Li-ion costs have fallen by more than 80% to create a mature and highly bankable technology that now has a proven track record in both utility scale and behind-the-meter applications. Project developers and investors often select Li-ion solutions as they offer faster returns, lower upfront capital and a highly competitive per-unit cost of storage.

This makes it difficult for LDES developers to compete in the same markets, despite being able to offer much larger storage durations. Current market dynamics don’t accurately price the benefits offered by these longer durations. As a result, policy support is often needed to make the economic case for LDES more favourable. Figure 3 shows LDES technologies mapped against cost and storage duration, with Li-ion based solutions being the cheapest.

Current policy support

The UK government has recognised the important role of long-duration storage by introducing a cap-and-floor mechanism to give LDES investors revenue certainty, with streams for both mature and emerging technologies. Under this revenue model, LDES projects are guaranteed a minimum floor price to protect against downside risk, while also agreeing to return revenues above an agreed price cap – to avoid excess windfalls.

In the first round, 171 projects were submitted, indicating strong industry momentum and developer interest in a mechanism that extends beyond short-term balancing markets. Despite this, some of the design details underpinning the mechanism are still to be determined and industry feedback has highlighted the importance of clarity around contract length and eligibility criteria. At the same time, there is discourse about the best way for the mechanism to interact with the existing capacity market and ancillary grid services to avoid distortion. If well-designed and implemented correctly, the cap-and-floor scheme could drive large-scale LDES deployment and ensure that renewable energy delivers its full potential in decarbonising the UK energy grid.

Future Outlook

Although still at an early stage, the UK is starting to advance large LDES projects, with many expected to benefit from the cap-and-floor scheme. For industry, thermal energy storage offers a route to decarbonising high-temperature production of steel, cement and chemicals – all areas where electrification alone cannot meet heat demands. Deploying TES at scale would reduce fossil fuel consumption in industrial clusters and reduce scope 1 emissions in sectors that are crucial to the UK economy.

More broadly, LDES could reshape the electricity market by providing storage over multi-day periods. These new technologies could create new value streams in capacity markets, reduce overall grid dependence on fossil fuels and lower curtailment costs associated with excess renewable generation. For investors and developers, LDES creates a new asset class with long-term revenue opportunities. Overall, the UK is an exciting hub of LDES technology advancement, with a strong policy support that is now supporting a growing pipeline of novel innovation.

[1] https://www.neso.energy/news/britains-electricity-explained-2024-review

[2] https://ember-energy.org/countries-and-regions/united-kingdom/

[4] https://www.neso.energy/publications/future-energy-scenarios-fes